Research in Options 2011

Bay of Angra dos Reis, Rio de Janeiro, de 26/11 até 01/12, 2011

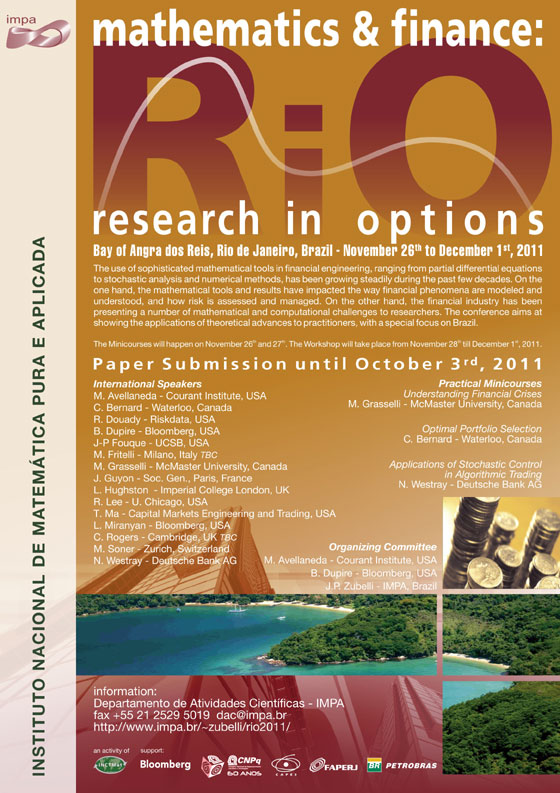

The use of sophisticated mathematical tools in financial engineering ranging from partial differential equations to stochastic analysis and numerical methods has been growing steadily during the past few decades. On the one hand, the mathematical tools and results have impacted the way financial phenomena are modeled and understood, and how risk is assessed and managed. On the other hand, the financial industry has been presenting a number of mathematical and computational challenges to researchers. The conference aims at showing the applications of theoretical advances to practitioners, with a special focus to Brazil.

This is the sixth conference hosted by IMPA’s group on Math Finance on the subject. It is a follow up of four highly successful previous ones. Each one had in its attendance about 100 participants evenly spread from academia and industry. This year we will focus on different aspects of option pricing ranging from fixed income and volatility trading to real options.

We will also have special sessions on risk management and portfolio optimization.

We will precede the conference with two days of minicourses. The minicourses will be aimed at practioners and students.

Paper submission extended untill October 31,2011.

Certificates

Organizing Committee

Marco Avellaneda – Courant Institute, USA

Bruno Dupire – Bloomberg, USA

Jorge Zubelli – IMPA, Brazil

International Speakers with Titles and Abstracts

Carole Bernard (Waterloo, Canada)

Minicourse: Optimal Portfolio Selection

Talk:Optimal investment under state-dependent constraints

John Chadam (University of Pittsburgh)

Talk: The Inverse Boundary Crossing Problem for Diffusions.

Raphael Douady (Riskdata, USA)

Talk: Nonlinear Polymodels and the StressVaR: New Risk Concepts for Fund Allocation

Bruno Dupire (Bloomberg, USA)

Talk: A New Approach to Volatility Derivatives

Jean-Pierre Fouque (UCSB, USA)

Talk: Smile at the Boundary Layer.

Matheus Grasselli (McMaster University, Canada)

Minicourse: Understanding financial crisis – a statistical perspective.

Talk: A dynamical systems model for credit expansion, asset price bubbles and financial fragility

Julien Guyon (Soc. Gen., Paris, France)

Talk: The smile calibration problem solved

Lane Hughston (Imperial College London, UK)

Talk: General Theory of Geometric Lévy Models for Dynamic Asset Pricing

Roger Lee (U. Chicago, USA)

Talk: Joint strike/expiry asymptotics of implied volatility

Terence Ma (Capital Markets Engineering and Trading, USA)

Talk: Repo 2008

Andreea Minca (Cornell University)

Talk: Credit default swaps and central clearing.

Luiza Miranyan (Bloomberg, USA)

Talk: On incorporating forward looking market data into linear multi-factor models

Chris Rogers (Cambridge, UK)

Talk: Market Selection: Hungry Misers and Happy Bankrupts

Martin Schweizer (ETH Zurich)

Talk: Stability aspects for absence of arbitrage conditions

Nicholas Westray (Deutsche Bank AG)

Minicourse: Applications of Stochastic Control in Algorithmic Trading

Talk: Global Markets Microstructure

Minicourses / Special Sessions

Matheus Grasselli (McMaster University, Canada)

Title: Understanding financial crisis – a statistical perspective.

Slide Presentation

Carole Bernard (Waterloo, Canada)

Title: Optimal Portfolio Selection

Slide Presentation

Nicholas Westray (Deutsche Bank AG)

Title: Applications of Stochastic Control in Algorithmic Trading

Slide Presentation

Contributed Communications

Edgardo Brigatti.

Title: Real Options: A Hedged Monte-Carlo Method.

Alan de Genaro (Bm&Fbovespa)

Title: Point Process in Finance: new results from an old acquaintance.

Ruth Kaila (Aalto University)

Title: Inverse problem of implied integrated variance, implied correlation coefficient, and implied interest rate.

Sandrine Tobelem-Foldvari (London School of Economics and Political Science)

Title: Autocorrelation and price impact in high frequency trades on the Johannesburg and Sao Paulo Stock Exchanges.

Diane Wilcox (University of The Witwatersrand)

Title: Autocorrelation and Price Impact in High Frequency Trades on the Johannesburg And Sao Paulo Stock Exchanges.

Poster Session

Juan Arismendi (Univ. of London)

Multivariate Truncated Moments.

Adriano De Cezaro (FURG)

Calibration of Local Volatility Surface by Iterative Methods.

Anastasia Ellanskaya (Université de Angers)

Indi erence pricing of the exponential Levy models.

Alexandru Hening (UCB)

Killed Brownian Motion with a Prescribed Lifetime Distribution and Models of Default.

Fabiana Travessini (FURG)

The Optimal Stopping Time in American Options: A Level Set Approach.

Juliano Melquiades Vianello / Marcela Lobo Francisco (Petróleo Brasileiro S/a (PETROBRAS) /Universidade Gama Filho (UGF))

Real Options Used in Projects of Industrial Unit Divided in Independent Subdivisions.

We will hold a poster session during part of the evenings so as to encourage the contribution of research and projects currently developed by students. Posters should be sent to math.fin.impa@gmail.com using Poster Session as subject. The standard adopted for posters is size A0 vertical.

Deadline for submission of posters: October 23rd, 2011.

Minicourse Schedule

Matheus Grasselli (McMaster University, Canada)

Title: Understanding financial crisis – a statistical perspective.

Slide Presentation

Carole Bernard (Waterloo, Canada)

Title: Optimal Portfolio Selection

Slide Presentation

Nicholas Westray (Deutsche Bank AG)

Title: Applications of Stochastic Control in Algorithmic Trading

Slide Presentation

Program

Special Session On Brazilian Markets

Marcos Carreira

Volatility – What is it for ?

Alan de Genaro

Generating Interest Rate Stress Scenarios

Pictures

Transportation

As you may know, Hotel do Bosque (where the conference will take place) is located in Mambucaba, Angra dos Reis, about 200 kilometers from Rio de Janeiro.

Transportation will be provided as follows:

Going to Hotel do Bosque – From Rio de Janeiro to Mambucaba

FRIDAY – NOV. 25

Bus 1 – The bus will leave from IMPA (Estrada Dona Castorina, 110 – Jardim Botanico) at 3 p.m, on November 25. The trip takes about 4 hours.

SUNDAY – NOV. 27

Bus 2 – The bus will leave from IMPA (Estrada Dona Castorina, 110 – Jardim Botanico) at 3 p.m., on November 27 , Sunday.

Back from Mambucaba to Rio de Janeiro

THURSDAY, DEC. 1

The bus will leave Hotel do Bosque on Thursday, December 1th, at 1:00 p.m. stopping at the international airport and the final stop will be at IMPA.

IMPORTANT: If you intend to use this service, please send us an e-mail to math.fin.impa@gmail.com confirming in which bus you would like to register.

Registered Participants

Hotel Reservation

Venue: Hotel do Bosque

IMPORTANT: Reservations to get the group rate should be made through our travel agent (gerencia@cmoeventos.com.br). Please do make a copy to math.fin.impa@gmail.com of such communications.

IMPORTANT NOTE TO INDUSTRY PARTICIPANTS: Please make your reservation asap. We cannot guarantee availability of hotel space for reservations after 14/11/2011. We urge you to make your reservation before this date.

IMPORTANTE: Reservas devem ser feitas o mais cedo possível. Após 14/11/2011 os quartos da reserva em bloco que efetuamos e que não foram utilizados serão liberados.

Event Webpage

Postal Address: Instituto Nacional de Matemática Pura e Aplicada

Estrada Dona Castorina 110, Jardim Botânico

Rio de Janeiro, RJ, CEP 22460-320, Brasil

E-mail: eventos@impa.br

{kind=link}

{kind=link}

{kind=link}

{kind=link}